Startup Valuation Explained: What Founders Need to Know

A practical look at how startup valuations are derived, and why the highest valuation is not always the best one.

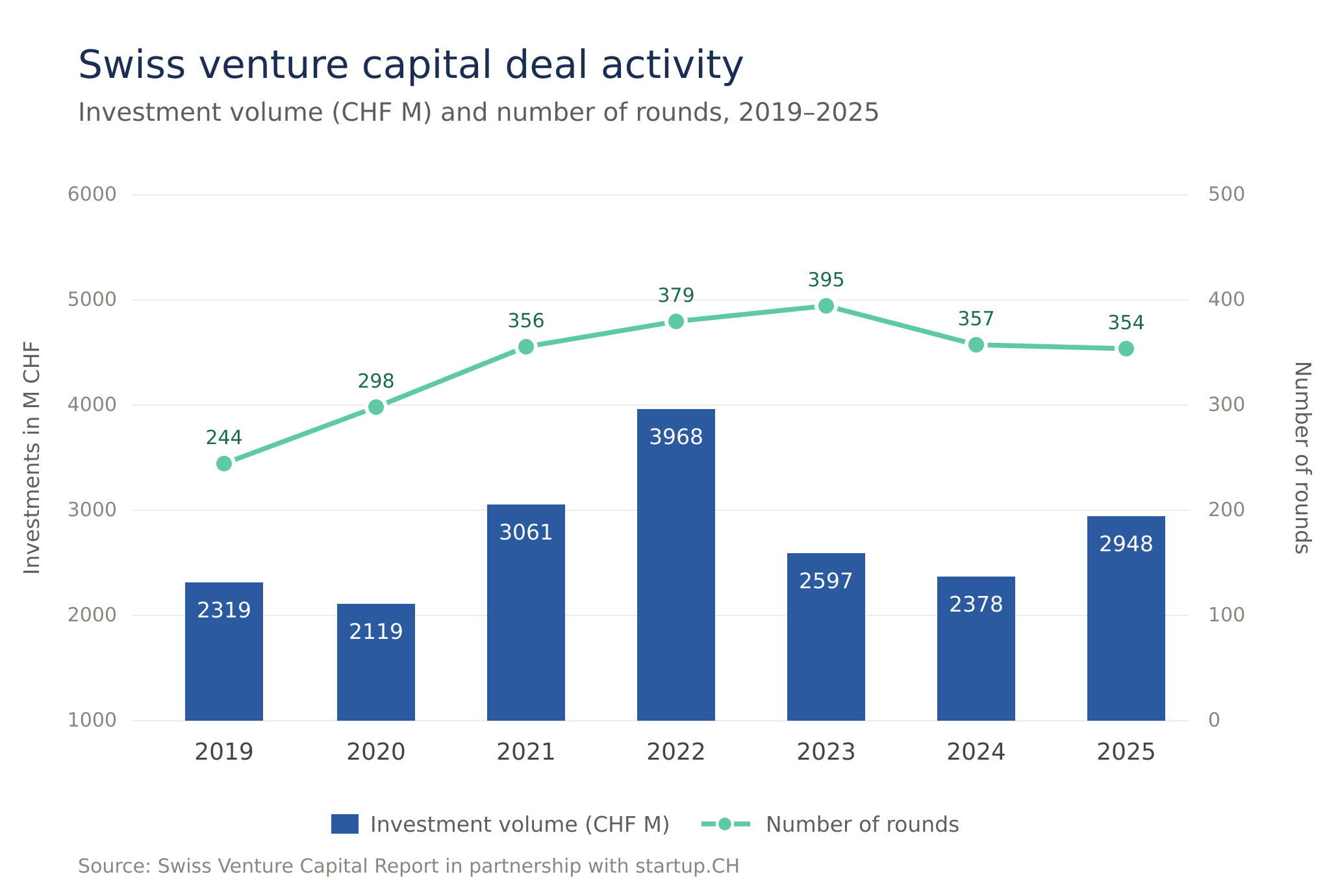

In 2025, Swiss startups raised CHF 2.9 billion across 354 financing rounds, up from CHF 2.4 billion across 357 rounds in 2024. In other words, more capital was deployed into slightly fewer rounds, a sign that fundraising momentum returned, but also that capital remained selective. Against that backdrop, valuation remains one of the most discussed and most misunderstood topics in startup finance. Because behind every funding headline sits the same question: How do founders and investors actually arrive at the number?

Valuation is not an exact science

Many founders look for one “correct” valuation. In practice, that number rarely exists.

Startup valuation is not just math. It is a mix of market evidence, financial logic, judgment, and negotiation. That is especially true at the early stage, where historical data is limited and future outcomes are highly uncertain.

That is why valuation is usually better understood as a range rather than a fixed truth. Two investors can look at the same company and arrive at different numbers, not because one of them is wrong, but because they underwrite risk, timing, and upside differently.

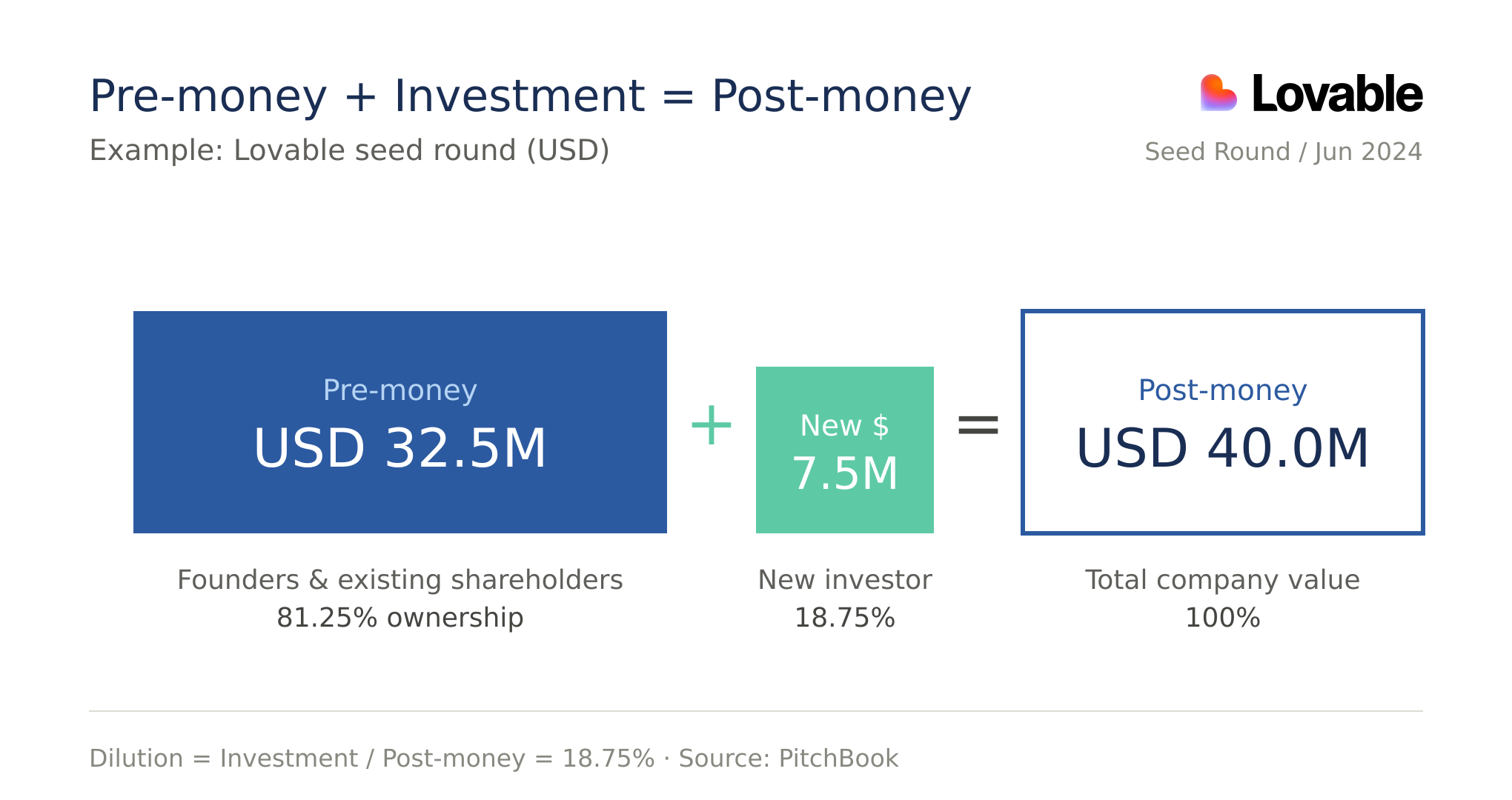

First, get the basics right: pre-money vs. post-money

Before discussing valuation methods, one basic concept needs to be clear: pre-money valuation is the agreed value of the company before the new investment. Post-money valuation is the pre-money valuation plus the investment amount. The difference directly determines dilution. Founders should make sure everyone is discussing the same basis from the start, which is usually the pre-money valuation.

Valuation is part of a bigger equation

Valuation does not exist in isolation. In a fundraising context, it is one variable within a broader financing construct: how much capital is raised, what dilution that implies, and whether the resulting runway is sufficient to reach the milestones required for the next round at a meaningful step-up.

In practice, rounds are typically engineered to fund 18–24 months of runway and to bridge the company to a clearly defined value inflection point, such as product-market fit, a revenue threshold, or regulatory approval. The valuation must be coherent with that trajectory. Too high, and the company risks a flat or down round if it cannot grow into the number. Too low, and founders give up unnecessary dilution. The strongest fundraising outcomes come from founders who treat valuation, raise, dilution, and milestones as an integrated system.

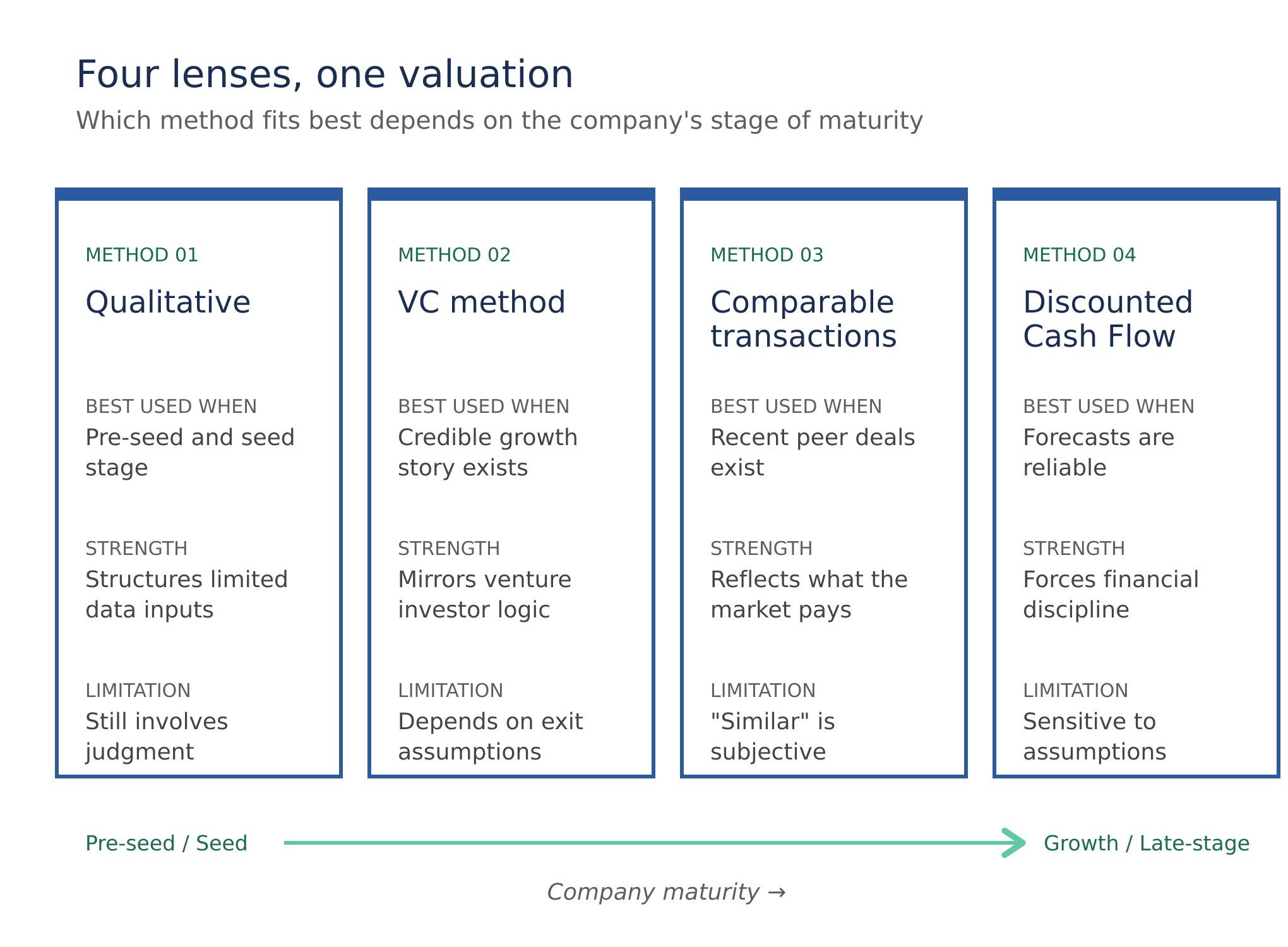

The main valuation methods

1) Qualitative methods

At pre-seed and seed stage, most startups are too early for detailed forecasting and too unique for clean market comparisons. Revenue, if any, says little about long-term potential. In those situations, investors and advisors rely on structured qualitative approaches.

One prominent example is a balanced scorecard. Rather than forcing precision from limited financial data, it scores the company across a defined set of dimensions and uses that structure to support the valuation discussion.

One example of how this qualitative logic can be formalised is BV4’s proprietary valuation model, developed in cooperation with the University of St. Gallen. It evaluates startups across more than 200 parameters within four critical dimensions: Team (e.g. founder complementarity, domain expertise, commitment), Product (e.g. stage of development, defensibility, IP position), Market (e.g. market size, growth dynamics, entry timing), and Business Model (e.g. scalability, unit economics, revenue quality).

2) VC Method

Once a startup has a credible growth story, the VC method becomes one of the most relevant tools. It takes a future-oriented view. Instead of focusing on what the company looks like today, it starts with an estimate of what the startup could realistically be worth at exit and then works backwards to today’s entry valuation, factoring in the returns venture investors require to compensate for early-stage risk.

In practice, investors do not only target a return multiple, they also target a minimum ownership stake, often between 10% and 20% across the investor syndicate, to ensure that a successful outcome can materially impact their portfolio.

This mirrors how many venture investors think, not just in terms of current performance, but in terms of how much value the company could create over time. Growth is therefore central, because it is one of the main drivers of a higher exit valuation and, consequently, of the investor’s return.

Simplified example: A SaaS startup projects CHF 50m ARR at exit in five years, valued at 5× ARR, resulting in CHF 250m. An investor committing CHF 5m today targets a 10× return, i.e. CHF 50m at exit. That implies the investor needs 20% of the company at exit and, assuming no further dilution, roughly a CHF 25m post-money valuation today.

In reality, founders should expect dilution from future rounds, which investors price in from the start, meaning the implied valuation today would typically be lower than this simplified version suggests.

Key takeaway: Valuation today is heavily influenced by how investors underwrite future dilution, exit scenarios, and portfolio return dynamics.

3) Comparable transactions

Comparable transactions are often the most intuitive method. The idea is simple: if similar startups at a similar stage have recently raised capital at a certain level, that creates a useful benchmark.

The challenge is that “similar” is doing a lot of work. Stage, geography, product maturity, business model, capital intensity, and investor appetite all matter. A Swiss B2B software company is not directly comparable to a US consumer app simply because both claim to be AI-driven.

At later stages, comparables can draw on more structured data points. Revenue multiples (e.g. EV/Revenue), customer metrics (e.g. ARR, net retention, CAC payback), and sector-specific benchmarks become increasingly available and allow for a more quantitative comparison with peers.

A good recent Swiss example is PAVE Space. In March 2026, the company raised USD 40 million in seed funding to develop orbital transfer vehicles for satellites. That does not mean every Swiss space-related deeptech company can anchor itself to a round of that size. But it does show how recent transactions shape the valuation corridor that founders and investors perceive as plausible in a given market window.

4) Discounted Cash Flow (DCF)

DCF becomes meaningful once a business has moved beyond pure potential. It is generally not applicable to pre-seed companies, where revenue trajectories are still speculative and margin structures unproven. Instead of asking what the market paid or what investors require, DCF asks what the business itself may be worth based on its own future cash flows.

In simple terms, the company projects future cash generation, estimates a long-term terminal value, and discounts everything back to today. The strength of DCF is that it forces discipline. It tests whether the business plan actually translates into future economics.

The weakness is just as important. Early-stage DCFs can look more precise than they really are. Small changes to the following metrics can materially alter the valuation:

- Growth projections

- Gross and EBITDA margins

- Market entry timing and adoption rate

- Discount rate

- Exit multiples

In other words, DCF is most powerful once a business has reached a stage where its financial trajectory can be modelled with a reasonable degree of confidence.

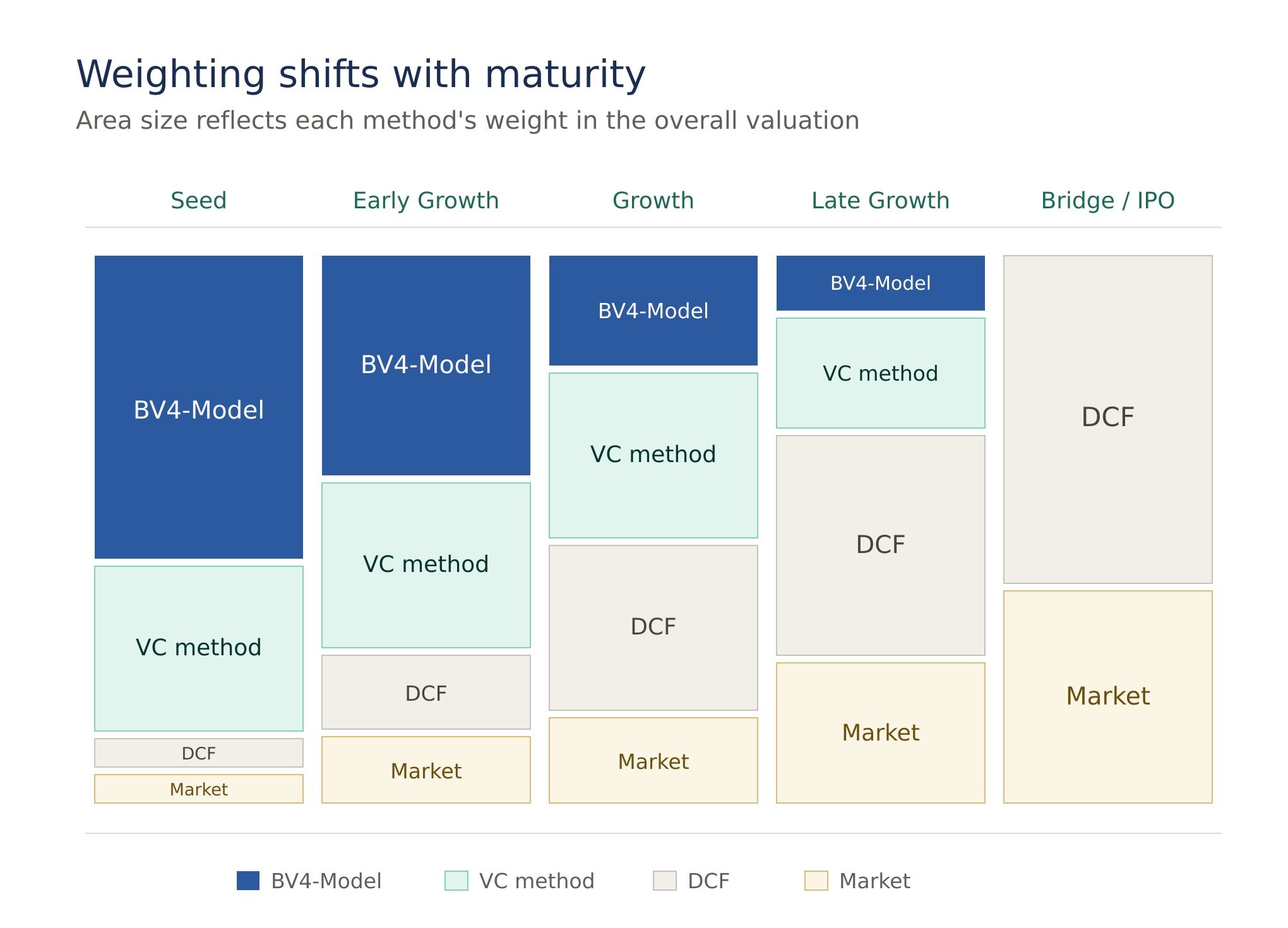

Why one method is usually not enough

No valuation method is perfect on its own.

Comparables are market-based but depend heavily on peer quality. DCF is financially grounded but highly assumption-driven. Qualitative methods are useful at early stage but inevitably subjective.

That is why strong startup valuations are usually built through triangulation. The goal is not to find one magical formula. The goal is to see whether several lenses broadly point in the same direction. If they do, confidence increases. If they do not, the gap itself tells you where the uncertainty lies.

In practice, this is also why BV4 typically delivers a valuation range rather than one fixed price. The relevance of each method depends on the company’s stage. Early-stage startups often require a stronger qualitative and venture-oriented lens, while later-stage companies can usually be assessed more robustly through comparables and DCF. By weighting the applicable methods accordingly, a valuation range can be derived, with the weighted average serving as an indication of fair market value. Especially in startup fundraising, a credible range is often more honest and more useful than pretending that one exact number captures the full reality of the business.

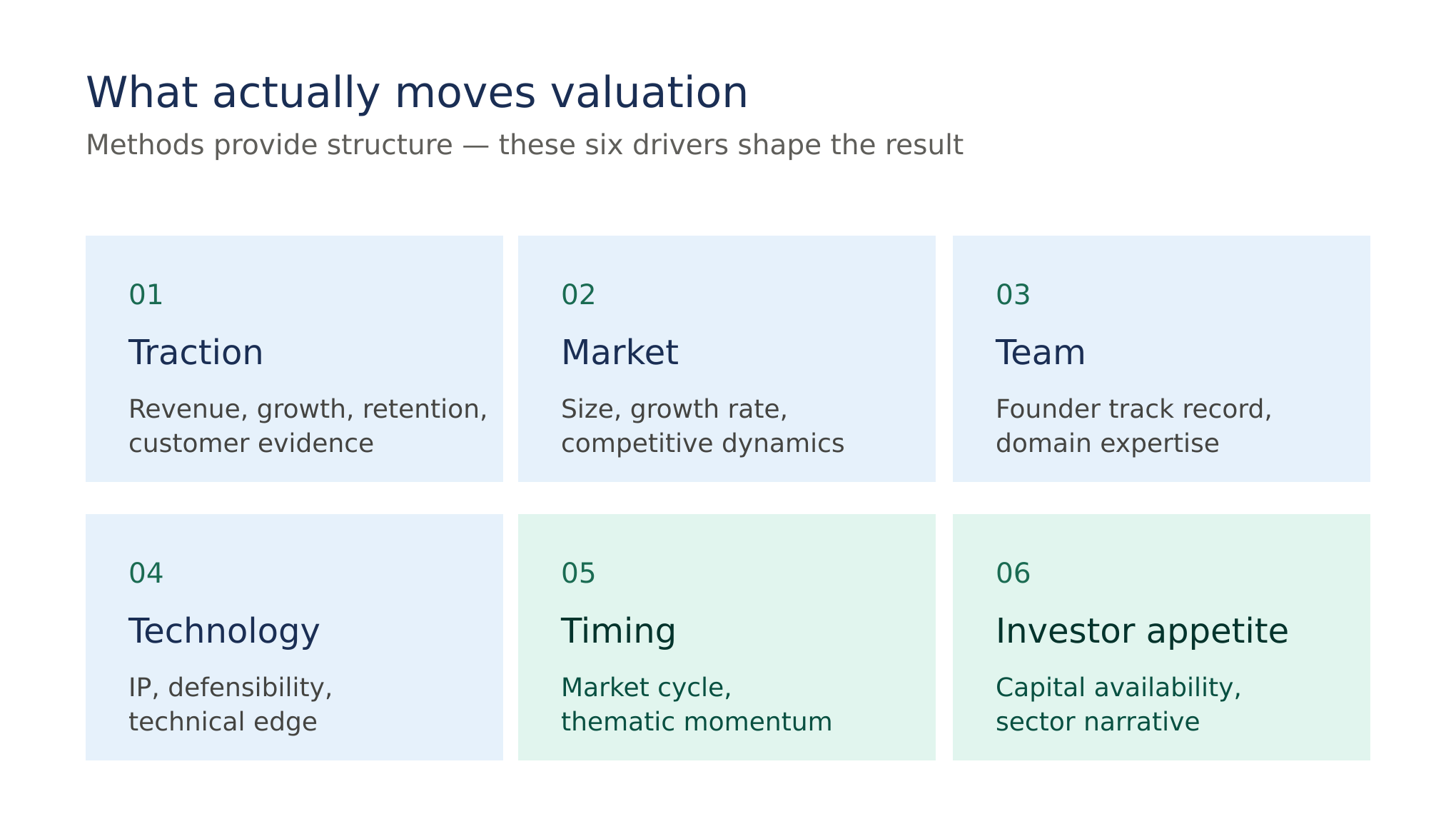

What influences the output?

Methods provide the structure. Market reality still shapes the result.

Traction matters. So do market size, team quality, technological edge, and unit economics. But timing matters more than is often acknowledged.

A recent Swiss example is AI. EY’s 2026 Swiss Start-up Barometer found that AI-based startups were involved in 32% of all Swiss funding rounds in 2025, while AI funding rose by 206% to around CHF 1.1 billion. That does not mean adding AI to a pitch deck automatically lifts valuation. But it does show how investor appetite, thematic momentum, and narrative can influence the final outcome.

Why high valuations can backfire

A high valuation is often treated as a win. Sometimes it is, but it can also create the wrong expectations.

If the company grows into that number, founders and investors look smart. If it does not, the next round can become much harder to close. That is why the best valuation is not always the highest one. It is the one that remains defensible when the market changes.

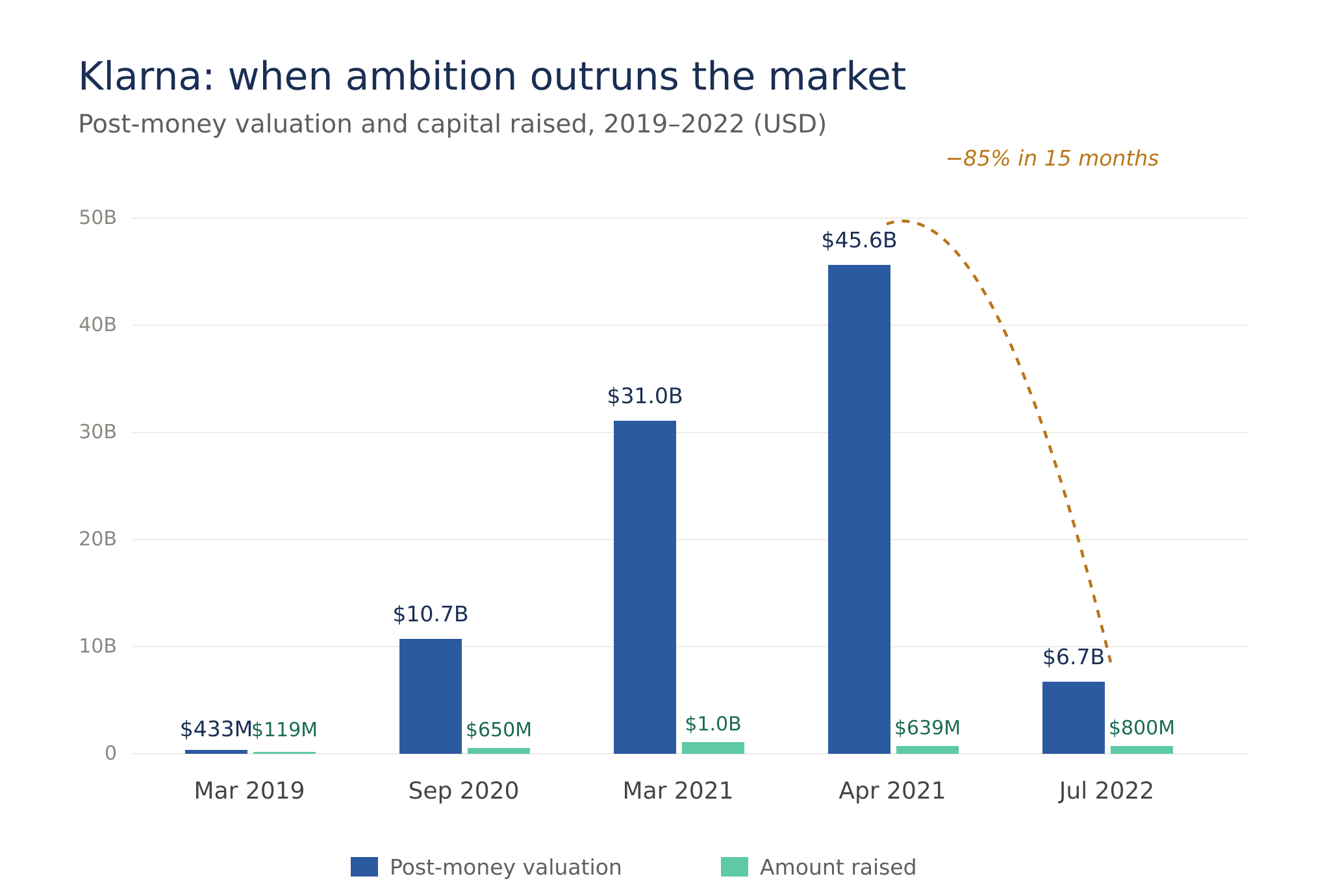

Klarna remains one of the clearest examples. In 2021, the company reached roughly a USD 46bn valuation. In July 2022, it raised USD 800m at a valuation of USD 6.7bn, an 85% drop. Reuters reported the reset in the context of a broader market pullback, while Klarna itself argued that public fintech peers were down 80–90% from their peak valuations. The lesson is not that founders should always be conservative. It is that ambitious valuations still need to be financeable in the next market environment, not only in the current one.

Conclusion

Startup valuation is not about finding one perfect number.

It is about using the right methods for the company’s stage, understanding what the market is willing to support, and having credible arguments to derive a fair market valuation.

For founders, that means two things: understand the logic and drivers behind the number, and remember that the best valuation is not necessarily the highest one. It is the one that helps you close the round with momentum, preserve credibility, and create room for the next stage of growth.

News

Other, related articles you may like